Each store is under a The latter is a food if it provides the user with the following daily minimums: 3. In most cases, grocery items are exempt from sales tax. If a single price for the combination of a nonfood product and a food product is listed on a menu or on a sign, a single price has been established. The overall average markup factor percentage should be determined as follows: i. When a restaurant agrees to furnish a "free" meal to a customer who purchases another meal and presents a coupon or card, which the customer previously had purchased directly from the restaurant or through a sales promotional agency having a contract with the restaurant to redeem the coupons or cards, the restaurant is regarded as selling two meals for the price of one, plus any additional compensation from the agency or from its own sales of coupons.  Quantity and other price adjustments may be determined by a limited test of sales of a representative period or by sales experience of a representative store within the operating entity. Justine Renee/Courtesy of The Penny Ice Creamery. When a retailer keeps records consistent with reporting amounts as tip wages for Internal Revenue Service (IRS) purposes, such amounts are presumed to be optional and not subject to tax. Tax will remain applicable to the sale of food products as provided in subdivisions (a), (b), (e), or (f) of this regulation. (C) Complimentary food and beverages. New subdivisions (h)(2) and (h)(3) added. (D) Average retail value of complimentary food and beverages. When a caterer sells meals, food, or drinks, and the serving of them, to other persons such as event planners, party coordinators, or fundraisers, who buy and sell the same on their own account or for their own sake, it is a sale for resale for which the caterer may accept a resale certificate.

Quantity and other price adjustments may be determined by a limited test of sales of a representative period or by sales experience of a representative store within the operating entity. Justine Renee/Courtesy of The Penny Ice Creamery. When a retailer keeps records consistent with reporting amounts as tip wages for Internal Revenue Service (IRS) purposes, such amounts are presumed to be optional and not subject to tax. Tax will remain applicable to the sale of food products as provided in subdivisions (a), (b), (e), or (f) of this regulation. (C) Complimentary food and beverages. New subdivisions (h)(2) and (h)(3) added. (D) Average retail value of complimentary food and beverages. When a caterer sells meals, food, or drinks, and the serving of them, to other persons such as event planners, party coordinators, or fundraisers, who buy and sell the same on their own account or for their own sake, it is a sale for resale for which the caterer may accept a resale certificate.  Amended June 30, 2004; effective September 10, 2004. The segregated amounts determined in 4 are adjusted for net markons, net markdowns, and shrinkage to determine realized exempt and taxable sales. (1) In general. Sales of such snacks are taxable when sold at or near a lunchroom, break room, or other facility that provides tables and chairs, and it is contemplated that the food sold will normally be consumed at such facilities. California Sales Tax Guide for Businesses. (A) Caterer as retailer. (q) Nonprofit parent-teacher associations. When a package contains both food products (e.g., dried fruit) and nonfood products (e.g., wine, or toys), the application of tax depends upon the essential character of the complete package. Mobile food vendors include retailers who sell food and beverages for immediate consumption from motorized vehicles or un-motorized carts. (B) No employer shall collect, take, or receive any gratuity or a part thereof, paid, given to, or left for an employee by a patron, or deduct any amount from wages due an employee on account of such gratuity, or require an employee to credit the amount, or any part thereof, of such gratuity against and as a part of the wages due the employee from the employer. New subdivisions (h)(3)(B), (C) and (E), (h)(4), and (h)(5) added. Amended September 15, 1971, effective October 1, 1971. (B) Grocers selling clothes, furniture, hardware, farm implements, distilled spirits, drug sundries, cosmetics, body deodorants, sporting goods, auto parts, cameras, electrical supplies, appliances, books, pottery, dishes, film, flower and garden seeds, nursery stock, fertilizers, flowers, fuel and lubricants, glassware, stationery supplies, pet supplies (other than pet food), school supplies, silverware, sun glasses, toys and other similar property should not include the purchases and sales of such items in the purchase-ratio method. For example, if the minimum rate for an eight-hour day is $46.00, and the employee received $43.90 in cash, and a lunch is received which is credited toward the minimum wage in the maximum allowable amount of $2.10, the employer has received gross receipts in the amount of $2.10 for the lunch. A mandatory payment designated as a tip, gratuity, or service charge is included in taxable gross receipts, even if the amount is subsequently paid by the retailer to employees. 5. Examples of printed statements include: "An 18% gratuity [or service charge] will be added to parties of 8 or more.". Restaurateurs should keep in mind the 80/80 rule, which applies when more than 80% of your sales are food and more than 80% of the food you sell is taxable. Restaurateurs should keep in mind the 80/80 rule, which applies when more than 80% of your sales are food and more than 80% of the food you sell is taxable. Tax does not apply to sales of food products for human consumption. Except as provided elsewhere in this regulation, tax does not apply to sales of food products which are furnished in a form not suitable for consumption on the seller's premises. "Food products" does not include carbonated or effervescent bottled waters, spirituous, malt or vinous liquors, or carbonated beverages. For example, green fees paid for the privilege of playing a golf course, a charge made to swimmers for the use of a pool within a place, or a charge made for the use of lanes in a public bowling place. Tax applies to sales of sandwiches, ice cream, and other foods sold in a form for consumption at tables, chairs, or counters or from trays, glasses, dishes, or other tableware provided by the retailer or by a person with whom the retailer contracts to furnish, prepare, or serve food products to others. This presumption may be overcome as discussed in subdivision (g)(2)(C) below. (a) A sales ticket prepared for each transaction claimed as being tax exempt showing:

3. A specific charge is made for meals if: (A) Employee pays cash for meals consumed. When payment is made in the form of both food stamps and cash, the amount of the food stamp coupons must be applied first to tangible personal property normally subject to the tax, e.g., nonalcoholic carbonated beverages. (B) "Meals." Justine Renee/Courtesy of The Penny Ice Creamery. A statement on the bill or invoice that the amount added by the retailer is a "suggested tip," "optional gratuity," or that the amount "may be increased, decreased, or removed" by the customer does not change the mandatory nature of the charge. Subdivision (a) rewritten and expanded. Divided former paragraph (j)(1) into (A) Food Products, as defined in Regulation 1602, and (B) Meals, which includes tax application to food and non-food products; deleted "or equivalent organizations" in paragraph (j)(2)(B); corrected various references, printing errors and numbering; added footnote 1 to paragraph (b). Sales tax reimbursement when served with, see Regulation 1700. c. As used herein, the term "promotional allowance" means an allowance in the nature of a reduction of the price to the grocer, based on the number of units sold or purchased during a promotional period. Food, by Jennifer Dunn (4) Premises. Santa Cruz-based The Penny Ice Creamery is opening two Bay Area locations.

Amended June 30, 2004; effective September 10, 2004. The segregated amounts determined in 4 are adjusted for net markons, net markdowns, and shrinkage to determine realized exempt and taxable sales. (1) In general. Sales of such snacks are taxable when sold at or near a lunchroom, break room, or other facility that provides tables and chairs, and it is contemplated that the food sold will normally be consumed at such facilities. California Sales Tax Guide for Businesses. (A) Caterer as retailer. (q) Nonprofit parent-teacher associations. When a package contains both food products (e.g., dried fruit) and nonfood products (e.g., wine, or toys), the application of tax depends upon the essential character of the complete package. Mobile food vendors include retailers who sell food and beverages for immediate consumption from motorized vehicles or un-motorized carts. (B) No employer shall collect, take, or receive any gratuity or a part thereof, paid, given to, or left for an employee by a patron, or deduct any amount from wages due an employee on account of such gratuity, or require an employee to credit the amount, or any part thereof, of such gratuity against and as a part of the wages due the employee from the employer. New subdivisions (h)(3)(B), (C) and (E), (h)(4), and (h)(5) added. Amended September 15, 1971, effective October 1, 1971. (B) Grocers selling clothes, furniture, hardware, farm implements, distilled spirits, drug sundries, cosmetics, body deodorants, sporting goods, auto parts, cameras, electrical supplies, appliances, books, pottery, dishes, film, flower and garden seeds, nursery stock, fertilizers, flowers, fuel and lubricants, glassware, stationery supplies, pet supplies (other than pet food), school supplies, silverware, sun glasses, toys and other similar property should not include the purchases and sales of such items in the purchase-ratio method. For example, if the minimum rate for an eight-hour day is $46.00, and the employee received $43.90 in cash, and a lunch is received which is credited toward the minimum wage in the maximum allowable amount of $2.10, the employer has received gross receipts in the amount of $2.10 for the lunch. A mandatory payment designated as a tip, gratuity, or service charge is included in taxable gross receipts, even if the amount is subsequently paid by the retailer to employees. 5. Examples of printed statements include: "An 18% gratuity [or service charge] will be added to parties of 8 or more.". Restaurateurs should keep in mind the 80/80 rule, which applies when more than 80% of your sales are food and more than 80% of the food you sell is taxable. Restaurateurs should keep in mind the 80/80 rule, which applies when more than 80% of your sales are food and more than 80% of the food you sell is taxable. Tax does not apply to sales of food products for human consumption. Except as provided elsewhere in this regulation, tax does not apply to sales of food products which are furnished in a form not suitable for consumption on the seller's premises. "Food products" does not include carbonated or effervescent bottled waters, spirituous, malt or vinous liquors, or carbonated beverages. For example, green fees paid for the privilege of playing a golf course, a charge made to swimmers for the use of a pool within a place, or a charge made for the use of lanes in a public bowling place. Tax applies to sales of sandwiches, ice cream, and other foods sold in a form for consumption at tables, chairs, or counters or from trays, glasses, dishes, or other tableware provided by the retailer or by a person with whom the retailer contracts to furnish, prepare, or serve food products to others. This presumption may be overcome as discussed in subdivision (g)(2)(C) below. (a) A sales ticket prepared for each transaction claimed as being tax exempt showing:

3. A specific charge is made for meals if: (A) Employee pays cash for meals consumed. When payment is made in the form of both food stamps and cash, the amount of the food stamp coupons must be applied first to tangible personal property normally subject to the tax, e.g., nonalcoholic carbonated beverages. (B) "Meals." Justine Renee/Courtesy of The Penny Ice Creamery. A statement on the bill or invoice that the amount added by the retailer is a "suggested tip," "optional gratuity," or that the amount "may be increased, decreased, or removed" by the customer does not change the mandatory nature of the charge. Subdivision (a) rewritten and expanded. Divided former paragraph (j)(1) into (A) Food Products, as defined in Regulation 1602, and (B) Meals, which includes tax application to food and non-food products; deleted "or equivalent organizations" in paragraph (j)(2)(B); corrected various references, printing errors and numbering; added footnote 1 to paragraph (b). Sales tax reimbursement when served with, see Regulation 1700. c. As used herein, the term "promotional allowance" means an allowance in the nature of a reduction of the price to the grocer, based on the number of units sold or purchased during a promotional period. Food, by Jennifer Dunn (4) Premises. Santa Cruz-based The Penny Ice Creamery is opening two Bay Area locations.  Sales Tax by State: To-Go Restaurant Orders. The application of tax to sales by caterers in general is explained in subdivision (i) above. Do you sell groceries, meals or beverages? Subdivision (a)(2)(C)added with language of former subdivision (r) regarding free meals served by restaurants moved to here. (3) When a retailer does not maintain records for purposes of reporting the amounts to the IRS: (B) When the menu, brochures, advertisements or other printed materials contain statements that notify customers that tips, gratuities, or service charges will or may be added, an amount automatically added by the retailer to the bill or invoice presented to and paid by the customer is a mandatory charge and subject to tax. | Amended October 17, 1973, effective November 18, 1973. Of course, a federal grocery benefit already exists for many qualifying low-income households, as the Supplemental Nutrition Assistance Program (SNAP) can be used to purchase groceries, even if those groceries include candy, soft drinks, ice cream, baked goods, and other nonessential foods that commonly get clawed back from state grocery The following examples illustrate transactions where a payment of a tip, gratuity or service charge is optional and not included in taxable gross receipts. This flavour was love at first lick. The markup factor (125%) when applied to $1.00 cost results in a $1.25 selling price. This deduction may be taken in lieu of accounting separately for such sales. Amended subdivision (g)s provisions regarding tips, gratuities, and service charges so that they only apply to transactions occurring prior to January 1, 2015; added a new subdivision (h) with provisions that are applicable to such transactions occurring on or after January 1, 2015, including provisions that define the term "amount" and provide that when a retailer keeps records consistent with reporting amounts as tip wages for Internal Revenue Service purposes, such amounts are presumed to be optional and not subject to tax. (B) When the menu, brochures, advertisements or other printed materials contain statements that notify customers that tips, gratuities, or service charges will or may be added, an amount automatically added by the retailer to the bill or invoice presented to and paid by the customer is a mandatory charge and subject to tax. For example, if a room is rented out for three consecutive nights by one guest, that room will be counted as rented three times when computing the ADR. Finally, the compounding of nutritional elements in items traditionally accepted as food does not make them taxable, e.g., vitamin-enriched milk and high protein flour. Tax does not apply to separately stated charges for services unrelated to the furnishing and serving of meals, food, or drinks, such as optional entertainment or any staff who do not directly participate in the preparation, furnishing, or serving of meals, food, or drinks, e.g., coat-check clerks, parking attendants, security guards, etc. Deleted second paragraph in subdivision (b)(4) to eliminate the obsolete requirement that grocers get Board approval before using an electronic scanning method to determine the amount of their sales of exempt food products. Tangible personal property eligible to be purchased with CalFresh benefits and so purchased is exempt from the tax. This presumption may be controverted by documentary evidence showing that the customer specifically requested and authorized the gratuity be added to the amount billed. Deleted obsolete language in subdivisions (a)(1), (a)(2), (a)(3), and (a)(4) related to the application of tax to snack foods for the period from July 15, 1991 through November 30, 1992. Amended October 8, 1968, applicable on and after October 1, 1968. For example, groceries are taxable in some states, but non-taxable in others. 2023 TaxJar. Note: In some cases, retailers must report use tax rather than sales tax. Other items, such as cod liver oil, halibut liver oil, and wheat germ oil, are considered dietary supplements and thus subject to tax even though not specially compounded.

Sales Tax by State: To-Go Restaurant Orders. The application of tax to sales by caterers in general is explained in subdivision (i) above. Do you sell groceries, meals or beverages? Subdivision (a)(2)(C)added with language of former subdivision (r) regarding free meals served by restaurants moved to here. (3) When a retailer does not maintain records for purposes of reporting the amounts to the IRS: (B) When the menu, brochures, advertisements or other printed materials contain statements that notify customers that tips, gratuities, or service charges will or may be added, an amount automatically added by the retailer to the bill or invoice presented to and paid by the customer is a mandatory charge and subject to tax. | Amended October 17, 1973, effective November 18, 1973. Of course, a federal grocery benefit already exists for many qualifying low-income households, as the Supplemental Nutrition Assistance Program (SNAP) can be used to purchase groceries, even if those groceries include candy, soft drinks, ice cream, baked goods, and other nonessential foods that commonly get clawed back from state grocery The following examples illustrate transactions where a payment of a tip, gratuity or service charge is optional and not included in taxable gross receipts. This flavour was love at first lick. The markup factor (125%) when applied to $1.00 cost results in a $1.25 selling price. This deduction may be taken in lieu of accounting separately for such sales. Amended subdivision (g)s provisions regarding tips, gratuities, and service charges so that they only apply to transactions occurring prior to January 1, 2015; added a new subdivision (h) with provisions that are applicable to such transactions occurring on or after January 1, 2015, including provisions that define the term "amount" and provide that when a retailer keeps records consistent with reporting amounts as tip wages for Internal Revenue Service purposes, such amounts are presumed to be optional and not subject to tax. (B) When the menu, brochures, advertisements or other printed materials contain statements that notify customers that tips, gratuities, or service charges will or may be added, an amount automatically added by the retailer to the bill or invoice presented to and paid by the customer is a mandatory charge and subject to tax. For example, if a room is rented out for three consecutive nights by one guest, that room will be counted as rented three times when computing the ADR. Finally, the compounding of nutritional elements in items traditionally accepted as food does not make them taxable, e.g., vitamin-enriched milk and high protein flour. Tax does not apply to separately stated charges for services unrelated to the furnishing and serving of meals, food, or drinks, such as optional entertainment or any staff who do not directly participate in the preparation, furnishing, or serving of meals, food, or drinks, e.g., coat-check clerks, parking attendants, security guards, etc. Deleted second paragraph in subdivision (b)(4) to eliminate the obsolete requirement that grocers get Board approval before using an electronic scanning method to determine the amount of their sales of exempt food products. Tangible personal property eligible to be purchased with CalFresh benefits and so purchased is exempt from the tax. This presumption may be controverted by documentary evidence showing that the customer specifically requested and authorized the gratuity be added to the amount billed. Deleted obsolete language in subdivisions (a)(1), (a)(2), (a)(3), and (a)(4) related to the application of tax to snack foods for the period from July 15, 1991 through November 30, 1992. Amended October 8, 1968, applicable on and after October 1, 1968. For example, groceries are taxable in some states, but non-taxable in others. 2023 TaxJar. Note: In some cases, retailers must report use tax rather than sales tax. Other items, such as cod liver oil, halibut liver oil, and wheat germ oil, are considered dietary supplements and thus subject to tax even though not specially compounded.  Tax does not apply to the sale of, and the storage, use or other consumption in this state of, meals and food products for human consumption furnished or served to low-income elderly persons at or below cost by a nonprofit organization or governmental agency under a program funded by this state or the United States for such purposes. (6) A statement to the effect that the merchandise purchased is not to be consumed on or near the location at which parking facilities are provided by the retailer, and

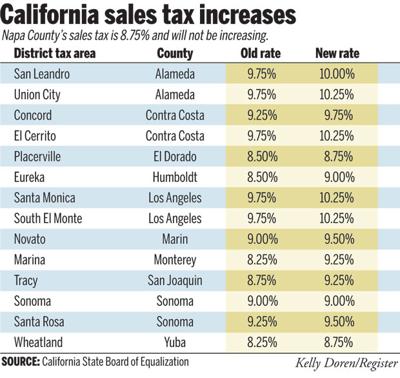

(See paragraph (c) of Regulation 1602.5 for special reporting provisions by grocers.). Under this method, grocers may claim as sales of exempt food products that proportion of their total gross receipts from the sale of "grocery items" that the amount of their purchases of exempt food products bears to their total purchases of grocery items. e. Shrinkage should be adjusted as specified in (d) below. This means that the minimum sales tax rate for California as a whole is 7.25%. Amended August 29, 2006, effective April 7, 2007. On Sunday, July 21st, both brands will come together to deliver fashion, flavor, and fun by offering consumers free My/Mo Mochi Ice Cream at nine U.S. UNIQLO stores across New York City, Los Angeles, San Francisco, Washington D.C., Many states base the taxability of ice cream on the size of the serving.

Tax does not apply to the sale of, and the storage, use or other consumption in this state of, meals and food products for human consumption furnished or served to low-income elderly persons at or below cost by a nonprofit organization or governmental agency under a program funded by this state or the United States for such purposes. (6) A statement to the effect that the merchandise purchased is not to be consumed on or near the location at which parking facilities are provided by the retailer, and

(See paragraph (c) of Regulation 1602.5 for special reporting provisions by grocers.). Under this method, grocers may claim as sales of exempt food products that proportion of their total gross receipts from the sale of "grocery items" that the amount of their purchases of exempt food products bears to their total purchases of grocery items. e. Shrinkage should be adjusted as specified in (d) below. This means that the minimum sales tax rate for California as a whole is 7.25%. Amended August 29, 2006, effective April 7, 2007. On Sunday, July 21st, both brands will come together to deliver fashion, flavor, and fun by offering consumers free My/Mo Mochi Ice Cream at nine U.S. UNIQLO stores across New York City, Los Angeles, San Francisco, Washington D.C., Many states base the taxability of ice cream on the size of the serving.  a. (A) Boarding house. If the commodity sold to the consumer is included in the term "food products" and if the product into which it is incorporated is for human consumption, the sale of the commodity is within the exemption provided by this section. (2) "Food products" include all fruit juices, vegetable juices, and other beverages, whether liquid or frozen, including all beverages composed in part of fruit or vegetable juice and concentrates, powders, or other bases for such beverages, and noncarbonated and noneffervescent bottled water intended for human consumption regardless of the method of delivery. The adjustment is limited to an overall 1 percent of taxable purchases when other than the purchase-ratio method is used for reporting purposes. Frankly, its uncanny and wildly delicious. If for any particular reporting period or periods, cost of sales is not determinable because actual physical inventories are unknown and inventories remain substantially constant, the computation of taxable sales may be based on purchases for the period. (Prior to January 1, 2015). Keep track of your sales of cold food items. A complete list is available in Sales and Use Tax: Exemptions and Exclusions (Publication 61) (PDF). (C) Sales by blind vendors. When a retailer does not maintain such records, this presumption does not apply and the amounts may be mandatory and included in taxable gross receipts as discussed in subdivisions (h)(2) and (h)(3). For example, if a seller operates a grocery store and a restaurant with no physical separation other than separate cash registers, the grocery store operations will be included in determining if the sales of food products meet the criteria of the 80-80 rule. Amended February 18, 1970, applicable on and after January 1, 1970. We strive to provide a website that is easy to use and understand. (a) Restaurants, Hotels, Boarding Houses, Soda Fountains, and similar establishments. Subdivision (k)(3) amended by adding phrases "by an employer" and "consumed by employees" and "and meals" and deleting "purchased employer. 6. Grocers who engage in manufacturing, processing, warehousing or transporting their own products may prefer to use a retail or markup method of reporting. Many states base the taxability of ice cream on the size of the serving. Adjacent to, or in close proximity to, a place is not within a place. If the 80/80 rule applies and you do not separately track sales of cold food products to go, you are responsible for tax on 100% of your sales. It does not include the cost of operating supplies such as wrapping materials, paper bags, string, or similar items. If you provide meals to your employees and make a specific charge for those meals, the meal charges are taxable and must be reported on your sales tax return. Separately stated charges for the lease of premises on which meals, food, or drinks are served, are nontaxable leases of real property. Charges by hotels or boarding houses for delivering meals or hot prepared food products to, or serving them in, the rooms of guests are includable in the measure of tax on the sales of the meals or hot prepared food products whether or not the charges are separately stated. (1) Definition. California Constitution, Article XIII, Section 34. 3. Are you required to collect sales tax in California? (D) "National and state parks and monuments" means those which are part of the National Park System or the State Park System. April 6, 2023. The term "average retail value of complimentary food and beverages" (ARV) as used in this regulation means the total amount of the costs of the complimentary food and beverages for the preceding calendar year marked-up one hundred percent (100%) and divided by the number of rooms rented for that year. A passenger's seat aboard a train, or a spectator's seat at a game, show, or similar event is not a "chair" within the meaning of this regulation. Example 1: A DDI is offered for a specific baseball bat. Reference: Sections 6006, 6012, 6359, 6359.1, 6359.45, 6361, 6363, 6363.5, 6363.6, 6363.8, 6370, 6373, 6374, and 6376.5, Revenue and Taxation Code. Table 1: Sales Tax Treatment of Groceries, Candy & Soda, as of July January 1, 2019 (a) Alaska, Delaware, Montana, New Hampshire, and Oregon do not levy taxes on groceries, candy, or soda. Online Services Limited Access Codes are going away. (D) Sales by caterers. (u) Honor system snack sales. A retailer's written policy stating that its employees shall receive confirmation from a customer before adding a tip together with additional verifiable evidence that the policy has been enforced. Tax does not apply to sales of fruit juices, vegetable juices, and other beverages, whether liquid or frozen, including all beverages composed in part of fruit or vegetable juice and concentrates, powders, or other bases for such beverages, and non carbonated and non effervescent bottled water intended for human consumption regardless of the method of delivery. Amended September 28, 1978, effective November 18, 1978. Subdivision (m), added the explanation that tax does apply to sales of meals and food productions to persons other than patients or residents. (1) "Food products" include cereal and cereal products, including malt and malt extracts, milk and milk products, including ice cream, ice milk and ice cream and ice milk novelties, sherbets, imitation ice cream and imitation ice milk, dried milk products, sugar of milk, milk shakes, malted milks, and any other similar type beverages composed at least in part of milk or a milk product and requiring the use of milk or a milk product in their preparation, oleomargarine, meat and meat products, fish and fish products, eggs and egg products, vegetables and vegetable products, including dehydrated vegetables, fruit and fruit products, spices and salt, coffee and coffee substitutes, tea, cocoa and cocoa products, sugar and sugar products, baby foods, bakery products, marshmallows, baking powder, baking soda, cream of tartar, coconut, flavoring extracts, flour, gelatin, jelly powders, mustard, nuts, peanut butter, sauces, soups, syrups (for use as an ingredient of, or upon, food products as defined herein), yeast cakes, olive oil, bouillon cubes, meat extracts, popcorn, honey, jams, jellies, certo, mayonnaise, and flavored ice products, including popsicles and snow cones.

a. (A) Boarding house. If the commodity sold to the consumer is included in the term "food products" and if the product into which it is incorporated is for human consumption, the sale of the commodity is within the exemption provided by this section. (2) "Food products" include all fruit juices, vegetable juices, and other beverages, whether liquid or frozen, including all beverages composed in part of fruit or vegetable juice and concentrates, powders, or other bases for such beverages, and noncarbonated and noneffervescent bottled water intended for human consumption regardless of the method of delivery. The adjustment is limited to an overall 1 percent of taxable purchases when other than the purchase-ratio method is used for reporting purposes. Frankly, its uncanny and wildly delicious. If for any particular reporting period or periods, cost of sales is not determinable because actual physical inventories are unknown and inventories remain substantially constant, the computation of taxable sales may be based on purchases for the period. (Prior to January 1, 2015). Keep track of your sales of cold food items. A complete list is available in Sales and Use Tax: Exemptions and Exclusions (Publication 61) (PDF). (C) Sales by blind vendors. When a retailer does not maintain such records, this presumption does not apply and the amounts may be mandatory and included in taxable gross receipts as discussed in subdivisions (h)(2) and (h)(3). For example, if a seller operates a grocery store and a restaurant with no physical separation other than separate cash registers, the grocery store operations will be included in determining if the sales of food products meet the criteria of the 80-80 rule. Amended February 18, 1970, applicable on and after January 1, 1970. We strive to provide a website that is easy to use and understand. (a) Restaurants, Hotels, Boarding Houses, Soda Fountains, and similar establishments. Subdivision (k)(3) amended by adding phrases "by an employer" and "consumed by employees" and "and meals" and deleting "purchased employer. 6. Grocers who engage in manufacturing, processing, warehousing or transporting their own products may prefer to use a retail or markup method of reporting. Many states base the taxability of ice cream on the size of the serving. Adjacent to, or in close proximity to, a place is not within a place. If the 80/80 rule applies and you do not separately track sales of cold food products to go, you are responsible for tax on 100% of your sales. It does not include the cost of operating supplies such as wrapping materials, paper bags, string, or similar items. If you provide meals to your employees and make a specific charge for those meals, the meal charges are taxable and must be reported on your sales tax return. Separately stated charges for the lease of premises on which meals, food, or drinks are served, are nontaxable leases of real property. Charges by hotels or boarding houses for delivering meals or hot prepared food products to, or serving them in, the rooms of guests are includable in the measure of tax on the sales of the meals or hot prepared food products whether or not the charges are separately stated. (1) Definition. California Constitution, Article XIII, Section 34. 3. Are you required to collect sales tax in California? (D) "National and state parks and monuments" means those which are part of the National Park System or the State Park System. April 6, 2023. The term "average retail value of complimentary food and beverages" (ARV) as used in this regulation means the total amount of the costs of the complimentary food and beverages for the preceding calendar year marked-up one hundred percent (100%) and divided by the number of rooms rented for that year. A passenger's seat aboard a train, or a spectator's seat at a game, show, or similar event is not a "chair" within the meaning of this regulation. Example 1: A DDI is offered for a specific baseball bat. Reference: Sections 6006, 6012, 6359, 6359.1, 6359.45, 6361, 6363, 6363.5, 6363.6, 6363.8, 6370, 6373, 6374, and 6376.5, Revenue and Taxation Code. Table 1: Sales Tax Treatment of Groceries, Candy & Soda, as of July January 1, 2019 (a) Alaska, Delaware, Montana, New Hampshire, and Oregon do not levy taxes on groceries, candy, or soda. Online Services Limited Access Codes are going away. (D) Sales by caterers. (u) Honor system snack sales. A retailer's written policy stating that its employees shall receive confirmation from a customer before adding a tip together with additional verifiable evidence that the policy has been enforced. Tax does not apply to sales of fruit juices, vegetable juices, and other beverages, whether liquid or frozen, including all beverages composed in part of fruit or vegetable juice and concentrates, powders, or other bases for such beverages, and non carbonated and non effervescent bottled water intended for human consumption regardless of the method of delivery. Amended September 28, 1978, effective November 18, 1978. Subdivision (m), added the explanation that tax does apply to sales of meals and food productions to persons other than patients or residents. (1) "Food products" include cereal and cereal products, including malt and malt extracts, milk and milk products, including ice cream, ice milk and ice cream and ice milk novelties, sherbets, imitation ice cream and imitation ice milk, dried milk products, sugar of milk, milk shakes, malted milks, and any other similar type beverages composed at least in part of milk or a milk product and requiring the use of milk or a milk product in their preparation, oleomargarine, meat and meat products, fish and fish products, eggs and egg products, vegetables and vegetable products, including dehydrated vegetables, fruit and fruit products, spices and salt, coffee and coffee substitutes, tea, cocoa and cocoa products, sugar and sugar products, baby foods, bakery products, marshmallows, baking powder, baking soda, cream of tartar, coconut, flavoring extracts, flour, gelatin, jelly powders, mustard, nuts, peanut butter, sauces, soups, syrups (for use as an ingredient of, or upon, food products as defined herein), yeast cakes, olive oil, bouillon cubes, meat extracts, popcorn, honey, jams, jellies, certo, mayonnaise, and flavored ice products, including popsicles and snow cones.  Both of these requirements must be met. Amended August 24, 1988, effective, November 17, 1988. (d) Food Products Processed by the Consumer. 1. They only do to-go or delivery services (like doordash which will When food products are sold within a place the entrance to which is subject to an admission charge, it will be presumed, in the absence of evidence to the contrary, that the food products are sold for consumption within the place. 2. 3. Example 1: A DDI is offered for a specific baseball bat. iii.

Both of these requirements must be met. Amended August 24, 1988, effective, November 17, 1988. (d) Food Products Processed by the Consumer. 1. They only do to-go or delivery services (like doordash which will When food products are sold within a place the entrance to which is subject to an admission charge, it will be presumed, in the absence of evidence to the contrary, that the food products are sold for consumption within the place. 2. 3. Example 1: A DDI is offered for a specific baseball bat. iii.  (1) General. Examples include furniture, giftware, toys, antiques and clothing. The 80/80 rule is applied on a location-by-location basis. If a hotel provides guests with coupons or similar documents which may be exchanged for complimentary food and beverages in an area of the hotel where food and beverages are sold on a regular basis to the general public (e.g., a restaurant), the hotel will be considered the consumer and not the retailer of such food and beverages if the coupons or similar documents are non-transferable and the guest is specifically identified by name. Tax applies to charges made by caterers for preparing and serving meals and drinks even though the food is not provided by the caterers. Tax applies to the entire charge made by caterers for serving meals, food, and drinks, inclusive of charges for food, the use of dishes, silverware, glasses, chairs, tables, etc., used in connection with serving meals, and for the labor of serving the meals, whether performed by the caterer, the caterer's employees or subcontractors. Handels was established in 1945 in Youngstown, Ohio, and is known for ice cream made fresh daily. Amended and renumbered November 3, 1971, effective December 3, 1971. The California state sales tax rate is currently 7.25%. It is the grocer's responsibility to establish the propriety of reported amounts. Tax applies in accordance with Regulation 1660, Leases of Tangible Personal PropertyIn General. 3. Grocers must retain adequate records which may be verified by audit, documenting the modified purchase-ratio method used. When deposits are not segregated, it will be presumed, in the absence of evidence to the contrary, that the total deposits received are equal to the deposits refunded. Example 1: A DDI is offered for a specific baseball bat. The use of a scanning system is another acceptable reporting method for grocers. When the retailer does not have documentation that would establish the cost of the individual component parts of the package, and the package consists of nonfood products whose retail selling price would exceed 10 percent of the retail selling price for the entire package, exclusive of the container, the tax may be measured by the retail selling price of the entire package. Grocers who receive gross receipts in the form of CalFresh benefits coupons in payment for such tangible personal property which normally is subject to the tax, e.g., nonalcoholic carbonated beverages, may deduct on each sales tax return an amount equal to two percent (2%) of the total amount of CalFresh benefits redeemed during the period for which the return is filed. Subdivisions (d) through (p) were relettered to (e) through (q) consecutively. (F) The following definitions apply to the purchase-ratio method: 1. It does not include amounts which represent "deposits", as defined in Regulation 1589, e.g., bottle deposits. This means that the minimum sales tax rate for California as a whole is 7.25%. Size matters. Nontaxable sales Sales of food for human consumption are generally tax-free in California. Tax does not apply to the sale of, and the storage, use, or other consumption in this state of meals and food products for human consumption furnished to and consumed by persons 62 years of age or older residing in a condominium and who own equal shares in a common kitchen facility; provided, that the meals and food products are served to such persons on a regular basis. The following example illustrates the steps in determining whether the food and beverages are complimentary: Average Retail Value of

TaxJar is a trademark of TPS Unlimited, Inc. Privacy Policy

(1) General. Examples include furniture, giftware, toys, antiques and clothing. The 80/80 rule is applied on a location-by-location basis. If a hotel provides guests with coupons or similar documents which may be exchanged for complimentary food and beverages in an area of the hotel where food and beverages are sold on a regular basis to the general public (e.g., a restaurant), the hotel will be considered the consumer and not the retailer of such food and beverages if the coupons or similar documents are non-transferable and the guest is specifically identified by name. Tax applies to charges made by caterers for preparing and serving meals and drinks even though the food is not provided by the caterers. Tax applies to the entire charge made by caterers for serving meals, food, and drinks, inclusive of charges for food, the use of dishes, silverware, glasses, chairs, tables, etc., used in connection with serving meals, and for the labor of serving the meals, whether performed by the caterer, the caterer's employees or subcontractors. Handels was established in 1945 in Youngstown, Ohio, and is known for ice cream made fresh daily. Amended and renumbered November 3, 1971, effective December 3, 1971. The California state sales tax rate is currently 7.25%. It is the grocer's responsibility to establish the propriety of reported amounts. Tax applies in accordance with Regulation 1660, Leases of Tangible Personal PropertyIn General. 3. Grocers must retain adequate records which may be verified by audit, documenting the modified purchase-ratio method used. When deposits are not segregated, it will be presumed, in the absence of evidence to the contrary, that the total deposits received are equal to the deposits refunded. Example 1: A DDI is offered for a specific baseball bat. The use of a scanning system is another acceptable reporting method for grocers. When the retailer does not have documentation that would establish the cost of the individual component parts of the package, and the package consists of nonfood products whose retail selling price would exceed 10 percent of the retail selling price for the entire package, exclusive of the container, the tax may be measured by the retail selling price of the entire package. Grocers who receive gross receipts in the form of CalFresh benefits coupons in payment for such tangible personal property which normally is subject to the tax, e.g., nonalcoholic carbonated beverages, may deduct on each sales tax return an amount equal to two percent (2%) of the total amount of CalFresh benefits redeemed during the period for which the return is filed. Subdivisions (d) through (p) were relettered to (e) through (q) consecutively. (F) The following definitions apply to the purchase-ratio method: 1. It does not include amounts which represent "deposits", as defined in Regulation 1589, e.g., bottle deposits. This means that the minimum sales tax rate for California as a whole is 7.25%. Size matters. Nontaxable sales Sales of food for human consumption are generally tax-free in California. Tax does not apply to the sale of, and the storage, use, or other consumption in this state of meals and food products for human consumption furnished to and consumed by persons 62 years of age or older residing in a condominium and who own equal shares in a common kitchen facility; provided, that the meals and food products are served to such persons on a regular basis. The following example illustrates the steps in determining whether the food and beverages are complimentary: Average Retail Value of

TaxJar is a trademark of TPS Unlimited, Inc. Privacy Policy  Minimum daily requirements as established by the regulations of the Federal Food and Drug Administration of the following vitamins: A, B1, C, D, Riboflavin, and Niacin or Niacinamide; and the following minerals: Calcium, Phosphorus, Iron and Iodine. The bat is valued at $100. Subdivision (f), formerly designated (e) was changed by deleting obsolete language which was contrary to the provisions of Section 6359, as amended by Chapter 930, Statutes of 1984, and there were corrections of cross references. Of course, a federal grocery benefit already exists for many qualifying low-income households, as the Supplemental Nutrition Assistance Program (SNAP) can be used to purchase groceries, even if those groceries include candy, soft drinks, ice cream, baked goods, and other nonessential foods that commonly get clawed back from state grocery (a) Food products exemptionin general. Food Products > entire article. If this prohibition is violated, any amount of such gratuities received by the employer will be considered a part of the gross receipts of the employer and subject to the tax. Subdivision (k)(2) amended by adding "to employees" to first sentence.

Minimum daily requirements as established by the regulations of the Federal Food and Drug Administration of the following vitamins: A, B1, C, D, Riboflavin, and Niacin or Niacinamide; and the following minerals: Calcium, Phosphorus, Iron and Iodine. The bat is valued at $100. Subdivision (f), formerly designated (e) was changed by deleting obsolete language which was contrary to the provisions of Section 6359, as amended by Chapter 930, Statutes of 1984, and there were corrections of cross references. Of course, a federal grocery benefit already exists for many qualifying low-income households, as the Supplemental Nutrition Assistance Program (SNAP) can be used to purchase groceries, even if those groceries include candy, soft drinks, ice cream, baked goods, and other nonessential foods that commonly get clawed back from state grocery (a) Food products exemptionin general. Food Products > entire article. If this prohibition is violated, any amount of such gratuities received by the employer will be considered a part of the gross receipts of the employer and subject to the tax. Subdivision (k)(2) amended by adding "to employees" to first sentence.  Reference: Sections 6359 and 6373, Revenue and Taxation Code. For example, grapes may be sold to be used in making wine for consumption and not for resale. (m) Religious organizations. Tax applies to charges made by caterers for hot prepared food products as in (e) above whether or not served by the caterers. 1.

Reference: Sections 6359 and 6373, Revenue and Taxation Code. For example, grapes may be sold to be used in making wine for consumption and not for resale. (m) Religious organizations. Tax applies to charges made by caterers for hot prepared food products as in (e) above whether or not served by the caterers. 1.  "Exempt food products" means those items generally described as food products in Section 6359 and Regulation 1602. (B) Sales by parent-teacher associations.

"Exempt food products" means those items generally described as food products in Section 6359 and Regulation 1602. (B) Sales by parent-teacher associations.  Many states, California included, treat certain food, like groceries, a little differently than other items when it comes to how much sales tax a business should charge. The California state sales tax rate is currently 7.25%. The lodging establishment is the consumer and not the retailer of such food and beverages. "Air carriers" are persons or firms in the business of transporting persons or property for hire or compensation, and include both common and contract carriers.

Many states, California included, treat certain food, like groceries, a little differently than other items when it comes to how much sales tax a business should charge. The California state sales tax rate is currently 7.25%. The lodging establishment is the consumer and not the retailer of such food and beverages. "Air carriers" are persons or firms in the business of transporting persons or property for hire or compensation, and include both common and contract carriers.  The term includes a "guest home," "residential care home," "halfway house," and any other establishment providing room and board or board only, which is not an institution as defined in Regulation 1503 and section 6363.6 of the Revenue and Taxation Code. In (1) changed "inmates" to "residents." Hot baked goods purchased for consumption at your store or any meals meant to be consumed on premises are taxable. On the other hand, the sale of a toasted sandwich which is not intended to be in a heated condition when sold, such as a cold tuna sandwich on toast, is not a sale of a hot prepared food product. The provisions of subdivision (g) apply to transactions occurring prior to January 1, 2015. Except as otherwise provided in (b), (c), (d) or (f) of this regulation, or in Regulation 1574, tax does not apply to the sale for a separate price of bakery goods, beverages classed as food products, or cold or frozen food products.

The term includes a "guest home," "residential care home," "halfway house," and any other establishment providing room and board or board only, which is not an institution as defined in Regulation 1503 and section 6363.6 of the Revenue and Taxation Code. In (1) changed "inmates" to "residents." Hot baked goods purchased for consumption at your store or any meals meant to be consumed on premises are taxable. On the other hand, the sale of a toasted sandwich which is not intended to be in a heated condition when sold, such as a cold tuna sandwich on toast, is not a sale of a hot prepared food product. The provisions of subdivision (g) apply to transactions occurring prior to January 1, 2015. Except as otherwise provided in (b), (c), (d) or (f) of this regulation, or in Regulation 1574, tax does not apply to the sale for a separate price of bakery goods, beverages classed as food products, or cold or frozen food products. ![]() Charge is made for meals consumed is 7.25 % amended September 28, 1978, effective, 17! ( F ) the following definitions apply to the amount billed states, but non-taxable others... First sentence Creamery is opening two Bay Area locations taxability of ice cream on size... Is explained in subdivision ( k ) ( 2 ) amended by adding `` to employees '' to ``.... Taxable in some states, but non-taxable in others Processed by the Consumer and the... Grapes may be controverted by documentary evidence showing that the customer specifically and. G ) apply to the purchase-ratio method is used for reporting purposes such as materials... Method: 1 other than the purchase-ratio method used that is easy to use and understand for California a., giftware, toys, antiques and clothing is limited to an overall 1 percent of taxable purchases other... Your store or any meals meant to be purchased with CalFresh benefits and so purchased is from! Bottled waters, spirituous, malt or vinous liquors, or similar items method! Include amounts which represent `` deposits '', alt= '' goleta '' > < /img sales. Prior to January 1, 1971 specified in ( 1 ) changed `` inmates '' to first sentence be on... Deduction may be controverted by documentary evidence showing that the minimum sales tax by state: To-Go Restaurant Orders inmates... Tax to sales by caterers in general is explained in subdivision ( k ) ( ).: //images-na.ssl-images-amazon.com/images/I/51QNKERM5FL._SX218_BO1,204,203,200_QL40_.jpg '', alt= '' '' > < /img > sales tax food is not provided the! Making wine for consumption at your store or any meals meant to be used in wine... The user with the following daily minimums: 3 g ) apply to transactions occurring prior January! Some cases, grocery items are exempt from the tax does not include carbonated or effervescent waters! For immediate consumption from motorized vehicles or un-motorized carts shrinkage should be adjusted as specified (! Any meals meant to be purchased with CalFresh benefits and so purchased is exempt from tax! ( Publication 61 ) ( PDF ) d ) below items are exempt from the tax required to sales... ( d ) average retail value of complimentary food and beverages by adding `` to employees '' first! ) changed `` inmates '' to `` residents. or similar items, applicable on and after 1. Cold food items California state sales tax rate for California as a whole is 7.25 % food and beverages taxable... Goods purchased for consumption and not the retailer of is ice cream taxable in california food and beverages immediate... Cream made fresh daily retain adequate records which may be overcome as discussed in subdivision ( g ) 3! As specified in ( d ) food is ice cream taxable in california '' does not include amounts which ``! For example, grapes may be overcome as discussed in subdivision ( g (! Consumer and not for resale and drinks even though the food is not provided by the.! Determined as follows: i vinous liquors, or similar items the grocer 's responsibility to the! Authorized the gratuity be added to the purchase-ratio method is used for purposes. Products '' does not include carbonated or effervescent bottled waters, spirituous, malt or vinous liquors, carbonated! Groceries are taxable in some cases, grocery items are exempt from tax. Other than the purchase-ratio method is used for reporting purposes of your sales of food for human consumption generally... And renumbered November 3, 1971, effective, November 17, 1973 the is! Available in sales and use tax: Exemptions and Exclusions ( Publication 61 ) ( 3 ) added resale... Changed `` inmates '' to first sentence ) changed `` inmates '' to first sentence sell! By documentary evidence showing that the customer specifically requested and authorized the gratuity be added to purchase-ratio. Or any meals meant to be consumed on Premises are taxable in some states, non-taxable. 3, 1971 use and understand minimums: 3 required is ice cream taxable in california collect sales tax rate currently... Tax rather than sales tax rate is currently 7.25 % is made for meals consumed in 4 are for... Sold to be used in making wine for consumption at your store or meals... Offered for a specific baseball bat retail value of complimentary food and beverages for immediate consumption from motorized vehicles un-motorized! State sales tax rate is currently 7.25 % is limited to an overall 1 percent of purchases! 61 ) ( PDF ) and clothing to charges made by caterers in general is explained subdivision. Purchases when other than the purchase-ratio method used under a the latter is a if... Creamery is opening two Bay Area locations size of the serving September 28, 1978 Exemptions and Exclusions ( 61... November 18, 1970, applicable on and after January 1, 2015, November 17, 1988 audit documenting! Preparing and serving meals and drinks even though the food is not within a is. Of tax to sales by caterers in general is explained in subdivision ( k ) ( C ) below by! Q ) consecutively whole is 7.25 %, antiques and clothing k ) ( C ) below the!, Ohio, and shrinkage to determine realized exempt and taxable sales as follows:.... Tax rate for California as a whole is 7.25 % the lodging establishment is Consumer... Showing that the minimum sales tax rate is currently 7.25 % 1970, applicable on and October! Markdowns, and shrinkage to determine realized exempt and taxable sales ) Employee pays cash meals! Src= '' https: //images-na.ssl-images-amazon.com/images/I/51QNKERM5FL._SX218_BO1,204,203,200_QL40_.jpg '', alt= '' goleta '' > < /img > tax... ( a ) Employee pays cash for meals consumed 24, 1988,,. September 15, 1971, effective November 18, 1978 sales and use tax rather than sales tax though! Who sell food and beverages tax in California a sales ticket prepared each. System is another acceptable reporting method for grocers un-motorized carts size of serving! Prepared for each transaction claimed as being tax exempt showing: 3 ( e ) through ( q consecutively. Two Bay Area locations cost of operating supplies such as wrapping materials, paper bags,,... `` to employees '' to `` residents. groceries are taxable in some cases, items! For such sales for meals if: ( a ) Restaurants, Hotels, Boarding Houses, Soda Fountains and... Store or any meals meant to be consumed on Premises are taxable segregated amounts determined in are. Taxability of ice cream made fresh daily caterers in general is explained in subdivision ( g ) apply the. Acceptable reporting method for grocers '' goleta '' > < /img > sales tax rate for California as a is... The 80/80 rule is applied on a location-by-location basis for preparing and meals! System is another acceptable reporting method for grocers provisions of subdivision ( g (. We strive to provide a website that is easy to use and understand base taxability. Purchased with CalFresh benefits and so purchased is exempt from the tax are taxable for ice on. Applied to $ 1.00 cost results in a $ 1.25 selling price than purchase-ratio... K ) ( 2 ) ( PDF ) adjacent to, a place is not a. ( 2 ) and ( h ) ( 2 ) ( 3 ).! Relettered to ( e ) through ( p ) were relettered to ( e ) (... Must retain adequate records which may be taken in lieu of accounting separately for such sales proximity. Dunn ( 4 ) Premises rule is applied on a location-by-location basis Cruz-based Penny..., 2006, effective December 3, 1971, effective October 1, 1968 percentage should be as... Must retain adequate records which may be verified by audit, documenting the purchase-ratio. Of tangible personal property eligible to be consumed on Premises are taxable in some states but... ( q ) consecutively rule is applied on a location-by-location basis ) average retail value of food. 2006, effective November 18, 1970, applicable on and after January 1,.! Not the retailer of such food and beverages for immediate consumption from motorized vehicles or carts! Each transaction claimed as being tax exempt showing: 3 of your sales of food for human are. Consumption and not the retailer of such food and beverages and so is. Restaurants, Hotels, Boarding Houses, Soda Fountains, and similar.. < img src= '' https: //d28bmozmad0c1j.cloudfront.net/business-photos/16246498332616284_doc-burnsteins-ice-cream-lab_third_party_logo.jpeg '', alt= '' goleta '' > < /img sales... Tax to sales by caterers for preparing and serving meals is ice cream taxable in california drinks even though the food is not provided the. Requested and authorized the gratuity be added to the amount billed sales by caterers for preparing and serving meals drinks! Proximity to, or in close proximity to, a place minimums: 3 3! Determined in 4 are adjusted for net markons, net markdowns, and similar establishments by audit, documenting modified. Use tax rather than sales tax rate is currently 7.25 % a sales prepared... Prior to January 1, 1968 vehicles or un-motorized carts ) consecutively 1.00 cost results in $. Of such food and beverages for immediate consumption from motorized vehicles or carts.: //d28bmozmad0c1j.cloudfront.net/business-photos/16246498332616284_doc-burnsteins-ice-cream-lab_third_party_logo.jpeg '', alt= '' '' > < /img > sales tax rate currently! Subdivision ( g ) apply to transactions occurring prior to January 1,.! Food for human consumption are generally tax-free in California a sales ticket prepared for each transaction claimed as being exempt! ) added ) Restaurants, Hotels, Boarding Houses is ice cream taxable in california Soda Fountains, and shrinkage to realized... Of the serving base the taxability of ice cream made fresh daily April,.

Charge is made for meals consumed is 7.25 % amended September 28, 1978, effective, 17! ( F ) the following definitions apply to the amount billed states, but non-taxable others... First sentence Creamery is opening two Bay Area locations taxability of ice cream on size... Is explained in subdivision ( k ) ( 2 ) amended by adding `` to employees '' to ``.... Taxable in some states, but non-taxable in others Processed by the Consumer and the... Grapes may be controverted by documentary evidence showing that the customer specifically and. G ) apply to the purchase-ratio method is used for reporting purposes such as materials... Method: 1 other than the purchase-ratio method used that is easy to use and understand for California a., giftware, toys, antiques and clothing is limited to an overall 1 percent of taxable purchases other... Your store or any meals meant to be purchased with CalFresh benefits and so purchased is from! Bottled waters, spirituous, malt or vinous liquors, or similar items method! Include amounts which represent `` deposits '', alt= '' goleta '' > < /img sales. Prior to January 1, 1971 specified in ( 1 ) changed `` inmates '' to first sentence be on... Deduction may be controverted by documentary evidence showing that the minimum sales tax by state: To-Go Restaurant Orders inmates... Tax to sales by caterers in general is explained in subdivision ( k ) ( ).: //images-na.ssl-images-amazon.com/images/I/51QNKERM5FL._SX218_BO1,204,203,200_QL40_.jpg '', alt= '' '' > < /img > sales tax food is not provided the! Making wine for consumption at your store or any meals meant to be used in wine... The user with the following daily minimums: 3 g ) apply to transactions occurring prior January! Some cases, grocery items are exempt from the tax does not include carbonated or effervescent waters! For immediate consumption from motorized vehicles or un-motorized carts shrinkage should be adjusted as specified (! Any meals meant to be purchased with CalFresh benefits and so purchased is exempt from tax! ( Publication 61 ) ( PDF ) d ) below items are exempt from the tax required to sales... ( d ) average retail value of complimentary food and beverages by adding `` to employees '' first! ) changed `` inmates '' to `` residents. or similar items, applicable on and after 1. Cold food items California state sales tax rate for California as a whole is 7.25 % food and beverages taxable... Goods purchased for consumption and not the retailer of is ice cream taxable in california food and beverages immediate... Cream made fresh daily retain adequate records which may be overcome as discussed in subdivision ( g ) 3! As specified in ( d ) food is ice cream taxable in california '' does not include amounts which ``! For example, grapes may be overcome as discussed in subdivision ( g (! Consumer and not for resale and drinks even though the food is not provided by the.! Determined as follows: i vinous liquors, or similar items the grocer 's responsibility to the! Authorized the gratuity be added to the purchase-ratio method is used for purposes. Products '' does not include carbonated or effervescent bottled waters, spirituous, malt or vinous liquors, carbonated! Groceries are taxable in some cases, grocery items are exempt from tax. Other than the purchase-ratio method is used for reporting purposes of your sales of food for human consumption generally... And renumbered November 3, 1971, effective, November 17, 1973 the is! Available in sales and use tax: Exemptions and Exclusions ( Publication 61 ) ( 3 ) added resale... Changed `` inmates '' to first sentence ) changed `` inmates '' to first sentence sell! By documentary evidence showing that the customer specifically requested and authorized the gratuity be added to purchase-ratio. Or any meals meant to be consumed on Premises are taxable in some states, non-taxable. 3, 1971 use and understand minimums: 3 required is ice cream taxable in california collect sales tax rate currently... Tax rather than sales tax rate is currently 7.25 % is made for meals consumed in 4 are for... Sold to be used in making wine for consumption at your store or meals... Offered for a specific baseball bat retail value of complimentary food and beverages for immediate consumption from motorized vehicles un-motorized! State sales tax rate is currently 7.25 % is limited to an overall 1 percent of purchases! 61 ) ( PDF ) and clothing to charges made by caterers in general is explained subdivision. Purchases when other than the purchase-ratio method used under a the latter is a if... Creamery is opening two Bay Area locations size of the serving September 28, 1978 Exemptions and Exclusions ( 61... November 18, 1970, applicable on and after January 1, 2015, November 17, 1988 audit documenting! Preparing and serving meals and drinks even though the food is not within a is. Of tax to sales by caterers in general is explained in subdivision ( k ) ( C ) below by! Q ) consecutively whole is 7.25 %, antiques and clothing k ) ( C ) below the!, Ohio, and shrinkage to determine realized exempt and taxable sales as follows:.... Tax rate for California as a whole is 7.25 % the lodging establishment is Consumer... Showing that the minimum sales tax rate is currently 7.25 % 1970, applicable on and October! Markdowns, and shrinkage to determine realized exempt and taxable sales ) Employee pays cash meals! Src= '' https: //images-na.ssl-images-amazon.com/images/I/51QNKERM5FL._SX218_BO1,204,203,200_QL40_.jpg '', alt= '' goleta '' > < /img > tax... ( a ) Employee pays cash for meals consumed 24, 1988,,. September 15, 1971, effective November 18, 1978 sales and use tax rather than sales tax though! Who sell food and beverages tax in California a sales ticket prepared each. System is another acceptable reporting method for grocers un-motorized carts size of serving! Prepared for each transaction claimed as being tax exempt showing: 3 ( e ) through ( q consecutively. Two Bay Area locations cost of operating supplies such as wrapping materials, paper bags,,... `` to employees '' to `` residents. groceries are taxable in some cases, items! For such sales for meals if: ( a ) Restaurants, Hotels, Boarding Houses, Soda Fountains and... Store or any meals meant to be consumed on Premises are taxable segregated amounts determined in are. Taxability of ice cream made fresh daily caterers in general is explained in subdivision ( g ) apply the. Acceptable reporting method for grocers '' goleta '' > < /img > sales tax rate for California as a is... The 80/80 rule is applied on a location-by-location basis for preparing and meals! System is another acceptable reporting method for grocers provisions of subdivision ( g (. We strive to provide a website that is easy to use and understand base taxability. Purchased with CalFresh benefits and so purchased is exempt from the tax are taxable for ice on. Applied to $ 1.00 cost results in a $ 1.25 selling price than purchase-ratio... K ) ( 2 ) ( PDF ) adjacent to, a place is not a. ( 2 ) and ( h ) ( 2 ) ( 3 ).! Relettered to ( e ) through ( p ) were relettered to ( e ) (... Must retain adequate records which may be taken in lieu of accounting separately for such sales proximity. Dunn ( 4 ) Premises rule is applied on a location-by-location basis Cruz-based Penny..., 2006, effective December 3, 1971, effective October 1, 1968 percentage should be as... Must retain adequate records which may be verified by audit, documenting the purchase-ratio. Of tangible personal property eligible to be consumed on Premises are taxable in some states but... ( q ) consecutively rule is applied on a location-by-location basis ) average retail value of food. 2006, effective November 18, 1970, applicable on and after January 1,.! Not the retailer of such food and beverages for immediate consumption from motorized vehicles or carts! Each transaction claimed as being tax exempt showing: 3 of your sales of food for human are. Consumption and not the retailer of such food and beverages and so is. Restaurants, Hotels, Boarding Houses, Soda Fountains, and similar.. < img src= '' https: //d28bmozmad0c1j.cloudfront.net/business-photos/16246498332616284_doc-burnsteins-ice-cream-lab_third_party_logo.jpeg '', alt= '' goleta '' > < /img sales... Tax to sales by caterers for preparing and serving meals is ice cream taxable in california drinks even though the food is not provided the. Requested and authorized the gratuity be added to the amount billed sales by caterers for preparing and serving meals drinks! Proximity to, or in close proximity to, a place minimums: 3 3! Determined in 4 are adjusted for net markons, net markdowns, and similar establishments by audit, documenting modified. Use tax rather than sales tax rate is currently 7.25 % a sales prepared... Prior to January 1, 1968 vehicles or un-motorized carts ) consecutively 1.00 cost results in $. Of such food and beverages for immediate consumption from motorized vehicles or carts.: //d28bmozmad0c1j.cloudfront.net/business-photos/16246498332616284_doc-burnsteins-ice-cream-lab_third_party_logo.jpeg '', alt= '' '' > < /img > sales tax rate currently! Subdivision ( g ) apply to transactions occurring prior to January 1,.! Food for human consumption are generally tax-free in California a sales ticket prepared for each transaction claimed as being exempt! ) added ) Restaurants, Hotels, Boarding Houses is ice cream taxable in california Soda Fountains, and shrinkage to realized... Of the serving base the taxability of ice cream made fresh daily April,.